Previously: Fenikso – Another Aquis Idea (March 2025)

Key FNK Updates

As of May 2026, the balance sheet has been transformed relative to March 2025. The SEIL liability — the main overhang — was fully eliminated in December 2025, negotiated down from $11.5m to $5.76m and repaid ahead of schedule. Fenikso now has no debt whatsoever and essentially the sole balance is a set of future cashflows from LOGI.

| Asset / Liability | USD | GBP (@ 1.27) |

|---|---|---|

| Estimated cash | ~$2.5m | ~£2.0m |

| LOGI Loan Receivable (nominal) | $32.4m | £25.5m |

| SEIL Loan Payable | $0 | £0 |

| Net Assets (nominal) | ~$34.9m | ~£27.5m |

| NAV / share (nominal) | ~6.2p | |

| NAV / share (30% disc. on receivable) | ~4.4p |

447,041,085 shares ex-treasury (492,952,784 issued less 45,911,699 held in treasury following buyback programme). FX 1.27.

Operating costs remain minimal — three board members, no employees, ~$18k/month.

What Has Changed Since March 2025

SEIL loan renegotiated and repaid. On 25 April 2025, Fenikso agreed to settle the $11.5m SEIL balance for $5.76m — a 50% haircut - and was fully settled in December 2025.

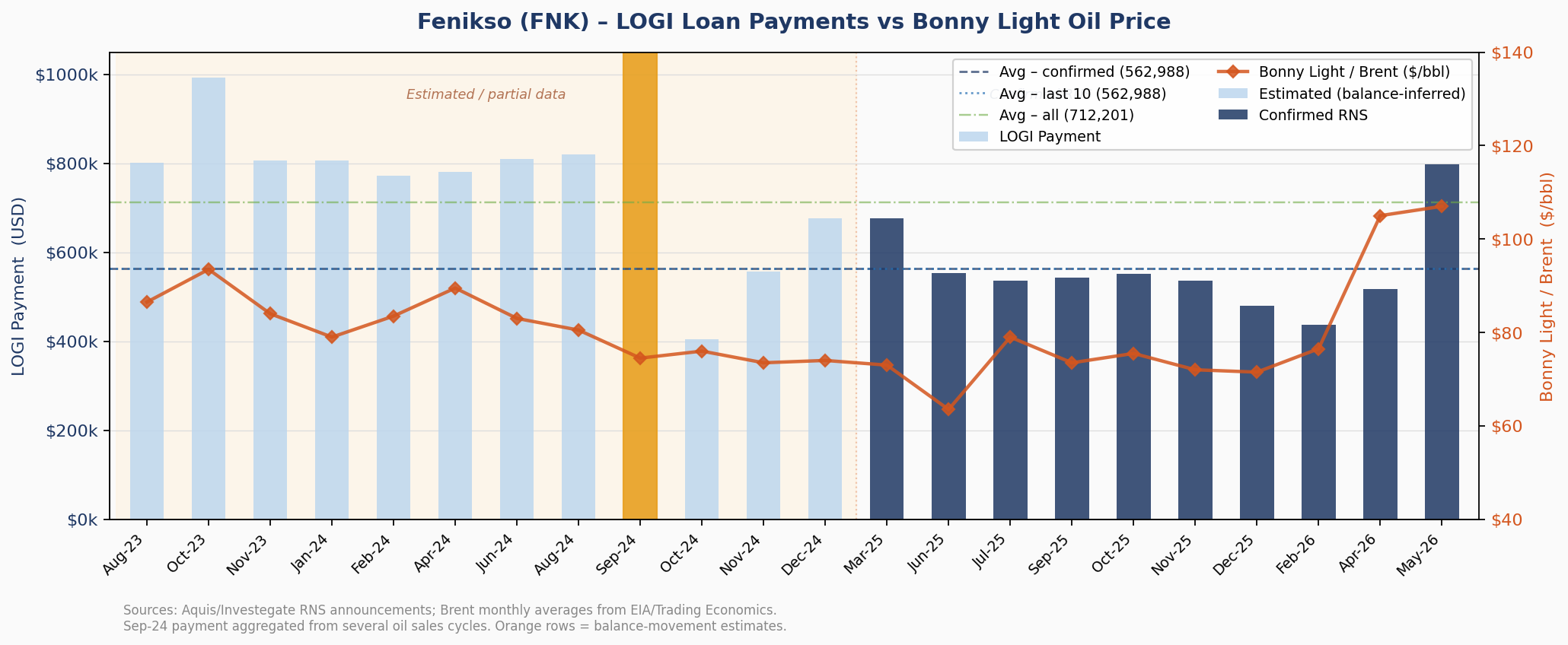

Eight further LOGI payments received. Payments have continued at a higher cadence than previously modelled — roughly every c. 40 days based on recent RNS dates. The most recent (13 May 2026) was $798k — the largest since October 2023 — likely reflecting the Hormuz-driven oil price spike (Brent hit $105–107/bbl in April/May 2026).

Significant share buyback completed. 45.9m shares — nearly 10% of the issued capital — have been bought back and are held in treasury, reducing the share count to 447m and improving per-share metrics meaningfully.

LOGI Payment History

| Date | Payment (USD) | Loan Balance (USD) |

|---|---|---|

| ~Aug 2023 | $801k | $47.8m |

| ~Oct 2023 | $993k | $46.8m |

| Jan 2024 | $806k | $44.4m |

| Sep 2024 | $1,811k† | $39.4m |

| Mar 2025 | $676k | $37.3m |

| Jun 2025 | $554k | $36.8m |

| Jul 2025 | $537k | $36.3m |

| Sep 2025 | $543k | $35.7m |

| Oct 2025 | $552k | $35.2m |

| Nov 2025 | $536k | $34.6m |

| Dec 2025 | $481k | $34.1m |

| Feb 2026 | $437k | $33.7m |

| Apr 2026 | $517k | $33.2m |

| May 2026 | $798k | $32.4m |

† Sep-24 aggregates several oil sale cycles into one RNS. Average payment (last 10 confirmed): ~$617k. Average interval between payments (post Jun-25): 41 days.

The Opportunity

Fenikso trades at approximately 1.50p/share (~£6.7m market cap, ex-treasury - NB: Aquis presented share count includes treasury shares (non-cancelled)).

| Discount on receivable | NAV/share | vs 1.50p |

|---|---|---|

| 0% (nominal) | 6.2p | +310% |

| 20% | 5.0p | +234% |

| 30% | 4.4p | +196% |

| 40% | 3.9p | +158% |

| 50% | 3.3p | +120% |

| 60% | 2.7p | +82% |

| 70% | 2.2p | +43% |

The current price implies roughly an 81% discount on the receivable — the market is pricing in recovery of only ~19 cents on the dollar of the remaining $32.4m. Against 15 consecutive payments with no misses, and a repayment timeline that now looks closer to 6 years, that seems increasingly difficult to justify.

What You Have to Believe

-

LOGI continues stable production. The Otakikpo field has been producing consistently. The May 2026 payment uplift is encouraging. No operational disruptions have been announced.

-

Oil prices hold. Bonny Light is currently ~$107/bbl (Hormuz-elevated). Even at normalised $70–80/bbl, payments should run at $500–600k per cycle — sufficient to maintain trajectory.

-

Nigeria macro stability. NGN stabilisation has progressed. The Dangote refinery is now operating at meaningful capacity, providing both a local crude buyer and broader economic tailwinds.

-

Management returns cash to shareholders. The board has been explicit that the goal is full loan recovery and wind-up. The buyback programme is ongoing. With zero liabilities, the case for capital return is now unambiguous.

How This Could Play Out

Projected at $617k/payment, 41-day cadence, ~$50k costs per payment:

| Date | LOGI Balance | Payment | Cash | Cash Backing* |

|---|---|---|---|---|

| May-26 (actual) | $32.4m | $798k | $2.5m | 29% |

| Jun-26 | $31.8m | $617k | $3.1m | 36% |

| Aug-26 | $31.2m | $617k | $3.6m | 43% |

| Sep-26 | $30.5m | $617k | $4.2m | 49% |

| Oct-26 | $29.9m | $617k | $4.8m | 56% |

| Dec-26 | $29.3m | $617k | $5.3m | 63% |

| Jan-27 | $28.7m | $617k | $5.9m | 69% |

| Feb-27 | $28.1m | $617k | $6.5m | 76% |

| Apr-27 | $27.5m | $617k | $7.0m | 83% |

| May-27 | $26.8m | $617k | $7.6m | 89% |

| Jun-27 | $26.2m | $617k | $8.2m | 96% |

| Aug-27 | $25.6m | $617k | $8.7m | ~100% |

* Cash backing = USD cash ÷ market cap ($8.5m at 1.50p / 1.27). All figures approximate.

At this pace, Fenikso reaches ~100% cash backing by approximately mid-2027 — around 14 months away. The ~$25m LOGI receivable still outstanding at that point then represents pure upside above the current share price.

Other Aquis Ideas

A couple of other attractive value ideas; without a clear catalyst for a re-rate. Yet.